What is the greek called Vega in options trading? How does options vega affect my options trading?

Options Vega - Definition

Options Vega measures the sensitivity of a stock option's price to a change in implied volatility.

Options Vega - Introduction

There are 2 main component to a stock option's price; Intrinsic Value and Extrinsic Value. The price of the underlying stock relative to the strike price determines the Intrinsic Value, which is governed by Options Delta. Implied volatility of the underlying stock determines the Extrinsic Value, which is governed by Options Vega. In fact, for Out Of The Money (OTM) Options that contains nothing more than extrinsic value, their prices are 100% determined by Options Vega! When implied volatility rises, the price of stock options rises along with it. Options Vega measures how much that rise is with every 1 percentage rise in implied volatility.

Why Is Options Vega Important?

It is almost impossible to understand why Options Vega is so important without first a comprehensive understanding of Implied Volatility.

Since implied volatility rises as important news releases approach and since Options Vega made sure that the price of the stock rises along with it, wouldn't the few days running up to such events be perfect for buying options and hoping that the stock remains relatively stagnant so as to profit from the rise in implied volatility? Yes! In fact, many options traders take delta neutral and gamma neutral positions a few days before important news releases so as to profit from the rise in implied volatility safely and then closing the position just before the release.

Just as implied volatility can float an option's price through Options Vega, it can also erase a big chunk of value off stock options very quickly should implied volatility falls dramatically, particularly after important news releases are made. This is what we call a Volatility Crunch. When implied volatility falls, options with positive Options Vega fall in value along with it. That is why it can be dangerous to buy options on stocks with a very high Options Vega just before important news releases if you want to hold that position for the long term. In fact, the implied volatility could have floated the extrinsic value of those options so high that when the big move is eventually made, it barely covers the extrinsic value and ends up in a loss all the same.

Options Vega - Characteristics

Positive And Negative Polarity

Options Vega come in positive or negative polarity. Long options produces positive Options Vega while short options produces negative Options Vega. Positive Options Vega increases the price of options and negative Options Vega decreases the value of that position when implied volatility goes up.

Options Vega & Options Moneyness

Options Vega decreases towards 0 as the option moves deeper In The Money or farther Out Of The Money. At The Money options typically has the highest Options Vega value. This also means that the extrinsic value of deep In The Money or far Out Of The Money options are less likely to change with a change in implied volatility. This is because stock options have lesser and lesser amount of extrinsic value as they move farther away from the money, and because Vega affects extrinsic value, it is natural for it to be lower at those points.

Learn about Options Moneyness now.

Options Vega & Time

Options Vega is higher as time to expiration becomes longer. The more time to expiration a stock option has, the more uncertainty there will be as to where it will end up by expiration, which translates into more opportunities for the buyer and higher risk for the seller. This results in a higher Vega for stock options with longer expiration in order to compensate for that additional risk taken by the seller.

Options Vega - Relationship with Options Gamma

Again, higher gains comes with higher risk. Like Options Theta, Options Vega also share a linear relationship with Options Gamma. When Options Gamma is highest, which is when options are At The Money, Options Vega is also the highest, subjecting the options trading position to a high risk of volatility crunch along with the potential of exponential, explosive gains granted by Gamma. With Vega as well as Theta working against an At The Money position, options traders need to make sure that the expected gain in the underlying stock more than covers the extrinsic value when buying such positions.

Options Vega - Selling Volatility

Now that we know Options Vega makes such a huge difference to extrinsic value through changes in implied volatility, one could also profit by "selling volatility". This is the writing of high Vega options during times of high implied volatility and then buying the position back after a volatility crunch. In fact, one could add insurance to such a position by ensuring that it is dynamically hedged to delta neutral through buying or selling the underlying stock.

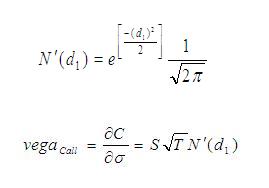

Options Vega Formula

The formula for calculation of option vega is:

Where...

d1 = Please refer to Delta Calculation

S = Current value of underlying asset

T = Option life as a percentage of year

C = Value of Call Option

Important Disclaimer : Options involve risk and are not suitable for all investors. Data and information is provided for informational purposes only, and is not intended for trading purposes. Neither www.optiontradingpedia.com, mastersoequity.com nor any of its data or content providers shall be liable for any errors, omissions, or delays in the content, or for any actions taken in reliance thereon. Data is deemed accurate but is not warranted or guaranteed. optiontradinpedia.com and mastersoequity.com are not a registered broker-dealer and does not endorse or recommend the services of any brokerage company. The brokerage company you select is solely responsible for its services to you. By accessing, viewing, or using this site in any way, you agree to be bound by the above conditions and disclaimers found on this site.

Copyright Warning : All contents and information presented here in www.optiontradingpedia.com are property of www.Optiontradingpedia.com and are not to be copied, redistributed or downloaded in any ways unless in accordance with our quoting policy. We have a comprehensive system to detect plagiarism and will take legal action against any individuals, websites or companies involved. We Take Our Copyright VERY Seriously!

Site Authored by