What Does Options Rho Represent in Options Trading?

Options Rho - Definition

Options Rho measures the sensitivity of a stock option's price to a change in interest rates.

Options Rho - Introduction

Options Rho is definitely the least important of the Options Greeks and have the least impact on stock options pricing. In fact, this is the options greek that is most often ignored by options traders because interest rates rarely change dramatically and the impact of such changes affect options price quite insignificantly. Options Rho measures the estimated change in the theoretical options price with a 1% change in Interest Rate and is often fairly low. This results in the price of a call option rising only about $0.01 or $0.02 with a 1% rise in interest rate, which is very insignificant.

Why Is Options Rho Unimportant?

Changes in interest rates dramatically affect the stock market and the economy. This makes it interesting to know how much the price of your options change with a change in interest rates through the Options Rho. However, changes in interest rates moves stocks more than is compensated by an increase or decrease in options price due to Options Rho. At the end of the day, Options Delta and Options Vega rule the day when interest rates changes or is expected to change soon. The impact of Options Rho could only be felt if all else remain stagnant in the face of something as important as a change in interest rates, which is nearly impossible. Even if you expect a change in interest rates and put on a position that is delta, vega, theta and gamma neutral (again, nearly impossible) in order to benefit from that $0.02 change, the transaction costs involved in such a complex hedge would have eradicated any possibility of real profits. On top of that, Options Rho is not usually needed for the calculation of any of the options trading strategies as there are currently no interest rates specific options trading strategies.

Options Rho - Characteristics

Positive And Negative Polarity

Options Rho come in positive or negative polarity. Long call options produces positive Options Rho and long put options produces negative Options Rho. This means that call options rise in value and put options drop in value with a rise in interest rates.

Options Rho & Time

Options Rho increases as time to expiration becomes longer.

Options Rho & Options Moneyness

Options Rho is almost equal for all In The Money options and decreases for Out Of The Money Options.

Typical Options Rho Value

Options Rho is usually in the 0.10 range for long expiration options and about the $0.010 range for near term options. This means that options with long expiration (LEAPS)are expected to rise by only $0.10 and near term options by only $0.01 with a 1% rise in interest rates. Both of which are fairly insignificant.

Options Rho - Why Does Put Options Have Negative Rho Value?

Stock Options buying are substitutions for the actual buying or shorting of the underlying stock. When you use all your cash to purchase shares, those cash no longer earn interest in your bank account. However, when you choose to control the same amount of shares using a much lower amount of money through the purchase of call options, the remaining cash continues to earn interest in your bank account. When interest rates rise, there is more incentive to keep more cash in bank accounts, making the purchase of call options more attractive than the purchase of shares. More attractive means more demand and more demand justifies a slightly higher price as measured by the options rho value. On the contrary, shorting shares put money into your bank account, earning interest. Put options as an alternative to shorting shares removed that benefit of having extra cash in your bank account in order to take advantage of rising interest rates. Thus in times of rising interest rates, investors move away from put options and into shorting the actual shares, thus creating a slight drop in demand for put options and hence the put options price. This creates the negative options rho value for put options while call options have positive rho values.

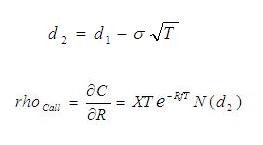

Options Rho Formula

The formula for calculation of option rho is:

Where...

d1 = Please refer to Delta Calculation

T = Option life as a percentage of year

C = Value of Call Option

X = Strike Price

N(d2) = Probability of option being in the money

|

Can't Decide Which Options Strategy To Use? Try our Option Strategy Selector! |

| Javascript Tree Menu |

Important Disclaimer : Options involve risk and are not suitable for all investors. Data and information is provided for informational purposes only, and is not intended for trading purposes. Neither www.optiontradingpedia.com, mastersoequity.com nor any of its data or content providers shall be liable for any errors, omissions, or delays in the content, or for any actions taken in reliance thereon. Data is deemed accurate but is not warranted or guaranteed. optiontradinpedia.com and mastersoequity.com are not a registered broker-dealer and does not endorse or recommend the services of any brokerage company. The brokerage company you select is solely responsible for its services to you. By accessing, viewing, or using this site in any way, you agree to be bound by the above conditions and disclaimers found on this site.

Copyright Warning : All contents and information presented here in www.optiontradingpedia.com are property of www.Optiontradingpedia.com and are not to be copied, redistributed or downloaded in any ways unless in accordance with our quoting policy. We have a comprehensive system to detect plagiarism and will take legal action against any individuals, websites or companies involved. We Take Our Copyright VERY Seriously!

Site Authored by